请老师帮忙看看我在闲鱼买的策略能否实盘交易?会信号闪烁吗?实盘能达到回测这样的效果吗?

//------------------------------------------------------------------------

// 简称: cdft

// 名称: 抄底反弹

// 类别: 公式应用

// 类型: 用户应用

// 输出: Void

//------------------------------------------------------------------------

Params

//此处添加参数

Numeric moneyRatio(0.1);

Numeric cd(0.001,0.001,0.01,0.001);

Numeric zy(0.005,0.0002,0.005,0.0001);

Numeric zs(0.005,0.0002,0.005,0.0001);

Vars

//此处添加变量

Numeric avg;

Global Numeric buyOpenPrice;

Global Numeric sellOpenPrice;

Global Integer timerId;

Defs

//此处添加公式函数

Numeric calcAvg(Numeric a,Numeric b)

{

return (a+b)/2;

}

Events

//此处实现事件函数

//初始化事件函数,策略运行期间,首先运行且只有一次,应用在订阅数据等操作

OnInit()

{

//timerId=createTimer(millsecs);

//与数据源有关

Range[0:DataCount-1]

{

//=========数据源相关设置==============

//AddDataFlag(Enum_Data_RolloverBackWard()); //设置后复权

//AddDataFlag(Enum_Data_RolloverRealPrice()); //设置映射真实价格

//AddDataFlag(Enum_Data_AutoSwapPosition()); //设置自动换仓

//AddDataFlag(Enum_Data_IgnoreSwapSignalCalc()); //设置忽略换仓信号计算

//AddDataFlag(Enum_Data_OnlyDay()); //设置仅日盘

//AddDataFlag(Enum_Data_OnlyNight()); //设置仅夜盘

//AddDataFlag(Enum_Data_NotGenReport()); //设置数据源不参与生成报告标志

//=========交易相关设置==============

//MarginRate rate;

//rate.ratioType = Enum_Rate_ByFillAmount; //设置保证金费率方式为成交金额百分比

//rate.longMarginRatio = 0.1; //设置保证金率为10%

//rate.shortMarginRatio = 0.2; //设置保证金率为20%

//SetMarginRate(rate);

//CommissionRate tCommissionRate;

//tCommissionRate.ratioType = Enum_Rate_ByFillAmount;

//tCommissionRate.openRatio = 5; //设置开仓手续费为成交金额的5%%

//tCommissionRate.closeRatio = 2; //设置平仓手续费为成交金额的2%%

//tCommissionRate.closeTodayRatio = 0; //设置平今手续费为0

//SetCommissionRate(tCommissionRate); //设置手续费率

//SetSlippage(Enum_Rate_PointPerHand,2); //设置滑点为2跳/手

//SetOrderPriceOffset(2); //设置委托价为叫买/卖价偏移2跳

//SetOrderMap2MainSymbol(); //设置委托映射到主力

//SetOrderMap2AppointedSymbol(symbols, multiples); //设置委托映射到指定合约,symbols是映射合约数组,multiples是映射倍数数组

}

//与数据源无关

//SetBeginBarMaxCount(10); //设置最大起始bar数为10

//SetBackBarMaxCount(10); //设置最大回溯bar数为10

//=========交易相关设置==============

SetInitCapital(1000000); //设置初始资金为100万

//AddTradeFlag(Enum_Trade_Ignore_Buy()); //设置忽略多开

//AddTradeFlag(Enum_Trade_Ignore_Sell()); //设置忽略多平

//AddTradeFlag(Enum_Trade_Ignore_SellShort()); //设置忽略空开

//AddTradeFlag(Enum_Trade_Ignore_Buy2Cover()); //设置忽略空平

}

//在所有的数据源准备完成后调用,应用在数据源的设置等操作

OnReady()

{

}

//基础数据更新事件函数

OnDic(StringRef dicName,StringRef dicSymbol,DicDataRef dicValue)

{

}

//在新bar的第一次执行之前调用一次,参数为新bar的图层数组

OnBarOpen(ArrayRef<Integer> indexs)

{

}

//Bar更新事件函数,参数indexs表示变化的数据源图层ID数组

OnBar(ArrayRef<Integer> indexs)

{

Numeric price;

Numeric a;

Numeric b;

Numeric c;

//avg=calcAvg(high,low);

Numeric df = Low/open-1;

Numeric hf = High/open-1;

//print(\"close1:\"+Text(Close[1])+\" close0:\"+Text(Close[0]));

if(MarketPosition==1){

Numeric zf = high/buyOpenPrice-1;

Numeric df = low/buyOpenPrice-1;

if (zf>=zy){

//Print(\"buyOpenPrice:\" + Text(buyOpenPrice));

price = buyOpenPrice*(1+zy);

Print(\"zy:\" + Text(price));

Sell(0,price);

}Else if (df<=-zs){

price = buyOpenPrice*(1-zs);

Print(\"zs:\" + Text(price));

Sell(0,price);

}

}

if(MarketPosition==-1){

Numeric zf = high/sellOpenPrice-1;

Numeric df = low/sellOpenPrice-1;

if (df<=-zy){

//Print(\"openPrice:\" + Text(openPrice));

price = sellOpenPrice*(1-zy);

Print(\"zy:\" + Text(price));

//Sell(0,price);

BuyToCover(0,price);

}Else if (zf>=zs){

price = sellOpenPrice*(1+zs);

Print(\"zs:\" + Text(price));

//Sell(0,price);

BuyToCover(0,price);

}

}

if(MarketPosition==0){

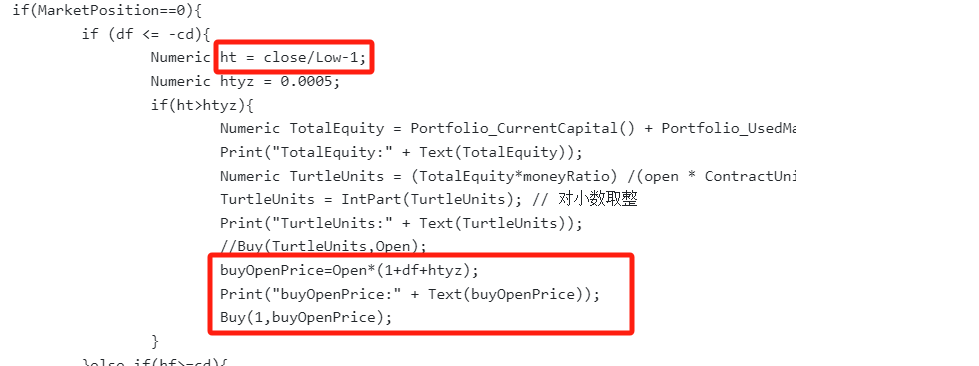

if (df <= -cd){

Numeric ht = close/Low-1;

Numeric htyz = 0.0005;

if(ht>htyz){

Numeric TotalEquity = Portfolio_CurrentCapital() + Portfolio_UsedMargin();

Print(\"TotalEquity:\" + Text(TotalEquity));

Numeric TurtleUnits = (TotalEquity*moneyRatio) /(open * ContractUnit()*BigPointValue()*MarginRatio());

TurtleUnits = IntPart(TurtleUnits); // 对小数取整

Print(\"TurtleUnits:\" + Text(TurtleUnits));

//Buy(TurtleUnits,Open);

buyOpenPrice=Open*(1+df+htyz);

Print(\"buyOpenPrice:\" + Text(buyOpenPrice));

Buy(1,buyOpenPrice);

}

}else if(hf>=cd){

Numeric ht = close/h-1;

Numeric htyz = 0.0005;

if(ht<-htyz){

Numeric TotalEquity = Portfolio_CurrentCapital() + Portfolio_UsedMargin();

Print(\"TotalEquity:\" + Text(TotalEquity));

Numeric TurtleUnits = (TotalEquity*moneyRatio) /(open * ContractUnit()*BigPointValue()*MarginRatio());

TurtleUnits = IntPart(TurtleUnits); // 对小数取整

Print(\"TurtleUnits:\" + Text(TurtleUnits));

//Buy(TurtleUnits,Open);

sellOpenPrice=Open*(1+hf-htyz);

Print(\"sellOpenPrice:\" + Text(sellOpenPrice));

//Buy(1,openPrice);

SellShort(1,sellOpenPrice);

}

}

}

}

//下一个Bar开始前,重新执行当前bar最后一次,参数为当前bar的图层数组

OnBarClose(ArrayRef<Integer> indexs)

{

}

//Tick更新事件函数,需要SubscribeTick函数订阅后触发,参数evtTick表示更新的tick结构体

OnTick(TickRef evtTick)

{

}

//持仓更新事件函数,参数pos表示更新的持仓结构体

OnPosition(PositionRef pos)

{

}

//策略账户仓更新事件函数,参数pos表示更新的账户仓结构体

OnStrategyPosition(PositionRef pos)

{

}

//委托更新事件函数,参数ord表示更新的委托结构体

OnOrder(OrderRef ord)

{

}

//成交更新事件函数,参数ordFill表示更新的成交结构体

OnFill(FillRef ordFill)

{

}

//定时器更新事件函数,参数id表示定时器的编号,millsecs表示定时间的间隔毫秒值

OnTimer(Integer id,Integer intervalMillsecs)

{

}

//通用事件触发函数,参数evtName为事件名称,参数evtValue为事件内容

OnEvent(StringRef evtName,MapRef<String,String> evtValue)

{

}

//当前策略退出时触发

OnExit()

{

}

假得不要不要的

一看回测图就知道偷价了,或有未来

官方不会评价用户间购买的程序,你可以直接找卖家

楼里也说了 存在偷价

计算使用close,用了未来数据;买入价格使用open相关,偷了数据。

实盘不可能会有如此平滑的曲线,要么有未来函数

看曲线就知道不能用,这么好的策略还用在闲鱼上卖?

我送你个无源码的给你,不要钱。

行啊,聯係方式方便説下嗎

tianxin_000456

微信吗

@wangkaiming老师帮忙看看,行吗

不能

现在真的是骗子无处不在

他的这个交易逻辑,能给我讲述下吗?我是个新手,

你的受骗策略,和我一样吗

不能用吗?